Winning With Strategic Options Winning With Strategic Options

If you don't know where you're going,

any option will get you there!

by Mark W. Sheffert

June 2009

You’ve got to be very careful if you don’t know where you are going, because you might not get there,” Yogi Berra, the former New York Yankees baseball player and manager, once said. His maxim suggests that without a sense of direction, we are lost and randomly wandering.

I’m afraid that’s the state of many companies right now, as we’ve all been hit hard with an economic knuckleball. If that feels familiar, perhaps you should explore your strategic options with a methodology that quantifies and qualifies the likely outcome of each option. If your strategic planning sessions are akin to throwing darts at a dartboard, the strategic-options analysis I propose will allow you to make informed decisions about your company’s organic growth, acquisitions, divestitures, or downsizing.

The best time to explore and assess strategic options is when the company is performing well. In other words, conduct a proactive study initiated by the board or management, instead of being forced to do so by a lender, investor group, or unfriendly acquirer. How many times have you read about a business in financial trouble that has hired an investment banking firm to help the company “explore its strategic options?” The truth is that it’s not really exploring strategic options, but is in a process to see how much the company can fetch in a distressed sale or a liquidation.

Different Planning Styles

Determining which strategy to use might depend in part on your leadership style. Business leaders create strategy, looking into the future and creating a map that shows where they are and where they want to be. But that’s when more knuckleballs are thrown at them. In competitive markets, no one can expect to formulate a detailed long-term plan and follow it mindlessly to the end.

Some business leaders seek to shape the future of their company with high-stakes bets, such as large acquisitions that will either make or break the company. I’m talking about a real toss of the dice—like Bank of America’s acquisition of Countrywide Financial. Only time will tell if that transaction will provide Bank of America with a robust mortgage banking and distribution channel, or a millstone around its neck.

Other business leaders who are more risk-averse may hedge their bets by making a few smaller acquisitions or investments. For example, to capitalize on growth opportunities in some emerging foreign markets, consumer-product companies have forged limited operational or distribution alliances.

Still other business leaders favor investments in flexibility that allow their companies to be nimble and adapt quickly as markets evolve. Unfortunately, the costs of establishing such flexibility can be high. Also, a wait-and-see strategy can turn into a fell-asleep-at-the-switch strategy, creating a window of opportunity for competitors.

Throwing Tradition Out the Window

With multiple options and differing leadership styles, how can leaders facing great uncertainty decide what’s best for their company? How should they decide whether to bet big, hedge, or wait and see?

Regrettably, using traditional strategic planning processes won’t help much in answering this question. The standard approach to analyzing strategic options is to use a discounted cash flow analysis. This method takes cash flow projections for a given investment and evaluates what the future value would be in present-day dollars. Changes are then made in key variables in an attempt to find the best outcome. Discounted cash flow helps companies determine the attractiveness of an investment.

This traditional approach may work in stable times, but in turbulent ones it’s only marginally helpful, and may be dangerously misleading. In my experience, strategic planning that requires rigid assumptions forces managers to bury underlying uncertainties in their projected cash flows. This pushes them to underestimate uncertainty to make a compelling case for their favorite strategy.

Try a New Approach

I’m suggesting a different approach to strategic decision making. Instead of guessing and politicking, go through a formal process to explore options, and quantify and qualify each of them, and then make a decision. An alternative approach incorporates the uncertain variables inherent in business and active decision making.

Which strategic model a company chooses is moot if the data that goes into it is invalid. Two strategic models that take into account change and turbulence are “real options valuation” (which looks at the value of a series of investments and factors in changes in price and demand) and “option games” (which incorporates game theory involving the competitor’s moves).

Present value (which compares the value of a dollar today to its value in the future, taking inflation and returns into account) and discounted cash flow use static cash flows to determine an outcome. For our purposes, I’m going to use discounted cash flow since it is the most universal method for determining investment decisions and valuations in businesses today, and a starting point for evaluating other strategies.

The key is to begin with an accurate cash flow forecast that anticipates uncertainties. Start by vetting the current budget for reality. This process may need to be performed by someone outside the company to assure objectivity. For instance, most budgets calculate a linear increase each year in revenues, expenses, and profits. However, if the company stops making capital investments, that could result in revenue actually declining as competitors gain an upper hand in the market.

Getting an objectively vetted “base case” is critical to beginning the process of examining strategic options. Once the base case of cash flow is determined, then future cash streams need to be discounted using the discounted cash flow model. Then you can calculate the present value using a discount interest rate (usually the company’s average cost of capital).

Intelligent Choices

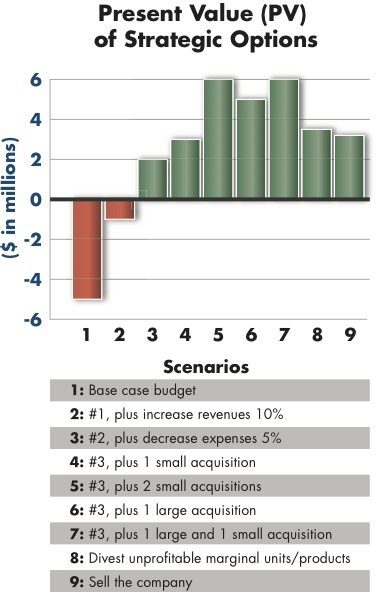

Now you can use the base case to determine what the present-value effect might be on the company’s future earnings. For example, if the company were to make a large acquisition of a major competitor, what would be the incremental gain in revenues? The expense take-outs? The resulting combined cash flow? What is the present value of this cash flow using various assumptions in a discounted cash flow model? As you can see in the graph below, by making a large acquisition, the company increases its incremental cash flow and present value significantly. However, this could also be a huge bet that the company has to weigh relative to the incremental gains.

This same process can also be used to examine other strategic options, such as acquiring one or two smaller competitors, or selling unprofitable divisions of the company. No matter which options you explore, think through the combinations and permutations that you would like to quantify, and challenge yourself to be realistic about the assumptions and uncertainties in each scenario.

This methodology quantifies and qualifies the likely outcome of each option, providing a solid basis for determining strategy and comparing and defending it against less attractive and less profitable options. Remember, Yogi also said, “90 percent of the game is half mental.”

Back to Top |